Jun 24, 2024

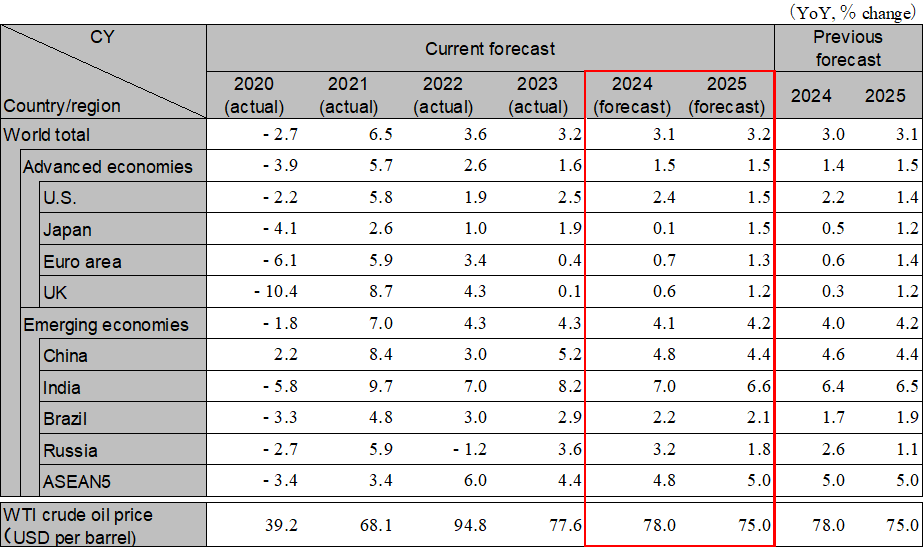

The global economy has so far shown greater tenacity than expected, despite uncertainties such as the deteriorating situation in the Middle East. In addition to the ongoing firmness of the U.S. economy that lies behind this, the immediate focus is on trends in inflation, which is still sticky, albeit on a slowing trend, and on U.S. monetary policy and global interest rate trends in response to this trend. Caution is still needed with regard to stagflation risk from renewed inflation and persistently high U.S. interest rates, sharp declines in emerging market currencies, and the risk of sudden changes in asset markets. The search for the sustainability of stable growth will continue, with its inherent fragility. Global growth is projected at 3.1% in 2024 and 3.2% in 2025.

U.S. GDP growth in January–March 2024 slowed from the previous quarter to +1.3% y/y, while employment data for April and May were mixed, but given a decline in the savings rate and a drop in new job openings, a further slowdown in the U.S. economy is expected in the second half of 2024. As for inflation, we expect the Fed to cut interest rates in September, as the pace of inflation is easing in some areas, such as services. Risks to the forecast include a slowdown in the economy due to prolonged high interest rates associated with high inflation and rising delinquency rates in commercial real estate and consumer loans. Real GDP growth is expected to be 2.4% in 2024 and 1.5% in 2025.

The Euro area GDP growth in January–March 2024 was +1.3% y/y, the highest in six quarters, and the economy is showing signs of recovery. Inflation continues to decline and the ECB cut interest rates in June 2024. The recovery is expected to accelerate in the second half of 2024 with the added effect of rate cuts. The UK also saw higher GDP growth in early 2024. Inflation continues to decline, and the BoE is expected to cut interest rates in August. A general election in July is expected to bring a change of government, but the economic impact will be limited. Real GDP growth in the Euro area will be 0.7% in 2024 and 1.3% in 2025. Real GDP growth in the UK is 0.6% in 2024 and is forecast to be 1.2% in 2025.

In China, last fall’s 1 trillion RMB fiscal stimulus package is having a positive effect, particularly in infrastructure construction related to flood control. Due to increased production and government support measures for GX, manufacturing investment also increases, and growth will continue through the second half of the year. Exports will continue to recover in a cyclical manner, although additional tariffs in the U.S. and Europe on EVs and other products will put downward pressure on exports. On the other hand, amid a sluggish employment environment, the recovery in consumption will remain slow. In real estate, the government expanded support measures to complete construction and adjust inventories, but on a limited scale, and the market normalization will be pushed back to 2025. Structural problems remain, including inadequate labor input and sluggish inward direct investment. Real GDP growth is projected to be 4.8% in 2024 and 4.4% in 2025.

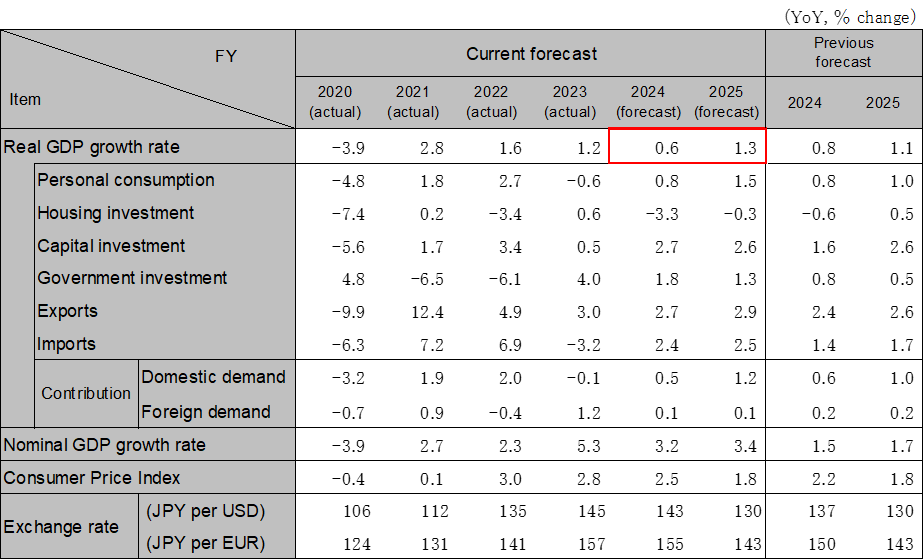

The Japanese economy is expected to gradually recover from the second half of 2024, thanks to the implementation of a fixed-amount tax reduction and the expansion of real wages, which will lead to a recovery in consumption. Regarding capital investment, it is expected to increase as large corporations, backed by high ordinary profits, take the lead. Although exports are expected to slow down in the first half of the year due to issues with an automotive fraud issue, they are expected to recover towards the end of the year due to increased demand resulting from interest rate cuts in Europe and the United States. While the BOJ may consider raising interest rates earlier depending on the future economic environment, it is expected to be implemented in October. The real GDP growth rate is expected to be 0.6% in FY2024 (0.1% in CY2024) and 1.3% in FY2025 (1.5% in CY2025).

India is expected to continue to grow at a high rate in FY2024, thanks to strong domestic demand, which is expected to be boosted by stable infrastructure investment as well as increased consumption due to slowing inflation. With stable inflation and a strong domestic economy, monetary policy is expected to remain unchanged for the time being. ASEAN is expected to recover in general due to a pickup in exports and inbound tourism, but caution is needed with regard to import inflation due to currency depreciation and rising food prices. Monetary policy varies from country to country; ASEAN-5 growth is expected to be 4.8% in 2024 and 5.0% in 2025.

Note:Values for Japan differ from those shown in the table below on a fiscal-year basis because they are on a calendar-year basis. However, India’s figures are shown on a fiscal-year basis. ASEAN5 is comprised of Indonesia, Thailand, Malaysia, the Philippines, and Vietnam.

Source: IMF, forecasts by Hitachi Research Institute

Note:The individual numbers and their sum may not match due to fractional processing.

Source: Cabinet Office, forecasts by Hitachi Research Institute

We provide you with the latest information on HRI‘s periodicals, such as our journal and economic forecasts, as well as reports, interviews, columns, and other information based on our research activities.

Hitachi Research Institute welcomes questions, consultations, and inquiries related to articles published in the "Hitachi Souken" Journal through our contact form.