~ Financial resilience and investment decisions amid heightened WACC volatility ~

May. 20, 2026

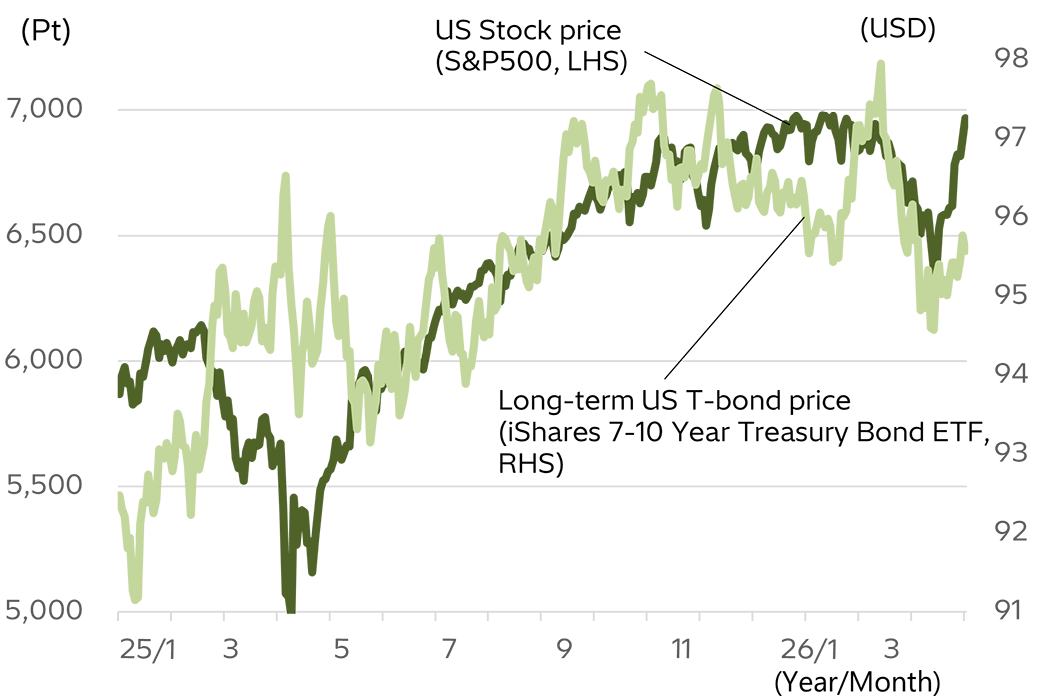

Figure 1: Trends in U.S. stock price and long-term Treasury bond price

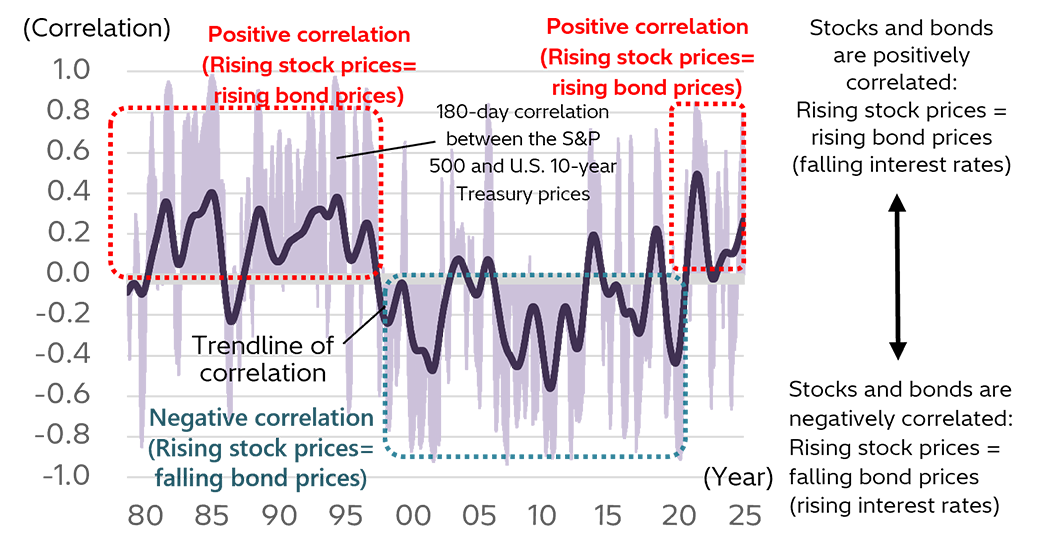

Figure 2: Correlation between U.S. stock prices and long-term Treasury bond prices

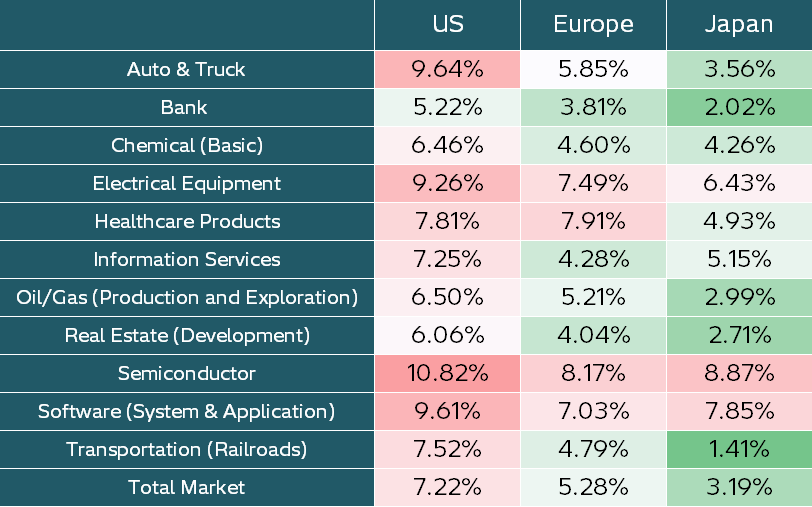

Table 1: WACC by region and industry (2025)

End of report

BIS (2023), “The correlation of equity and bond returns”, BIS Quarterly Review: December 4, 2023.

Damodaran, A.(2026), Damodaran Online, NYU Data history

IMF (2026), “Stock‑Bond Diversification Offers Less Protection from Market Selloffs”, IMF Blog, February 18, 2026

Kenichiro Yoshida

Chief Researcher, Global Intelligence and Research Office, Hitachi Research Institute

Engaged in research on economic and financial conditions in the United States and Europe. After graduating from Hitotsubashi University's Faculty of Commerce, he worked at Mizuho Research Institute and served as the Chief Representative of Mizuho Research Institute's London Office before assuming his current position in 2021.

Author’s Introduction

Kenichiro Yoshida

Chief Researcher

Global Intelligence and Research Office

We provide you with the latest information on HRI‘s periodicals, such as our journal and economic forecasts, as well as reports, interviews, columns, and other information based on our research activities.

Hitachi Research Institute welcomes questions, consultations, and inquiries related to articles published in the "Hitachi Souken" Journal through our contact form.