Feb. 27, 2026

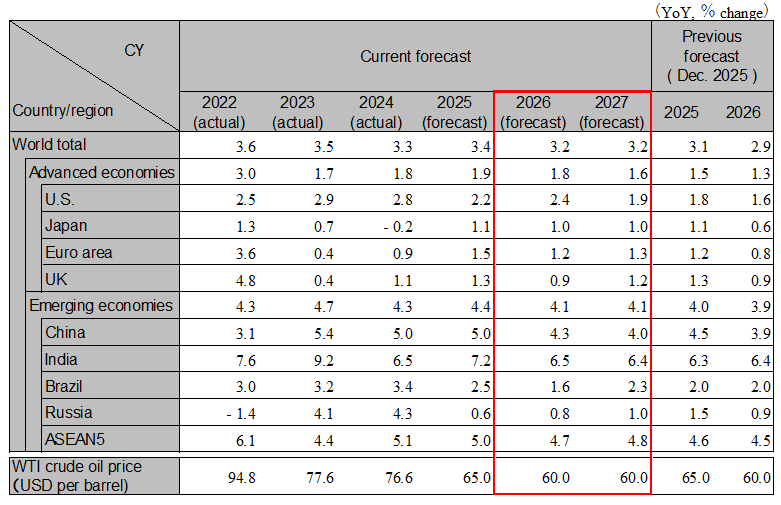

The global economy in 2026 started in a stable phase. However, tariff-related issues have resurfaced following a Supreme Court ruling that deemed certain measures unconstitutional. While trade frictions may re‑emerge intermittently, an extreme escalation is not expected. Supported by increased investment, expansionary fiscal policies, and accommodative monetary conditions, the main scenario is steady growth in the 3% range. At the same time, risks of economic and market instability remain, including a sharp equity sell-off driven by fading growth expectations for AI-related companies and excessive U.S. government intervention in areas such as monetary policy and corporate management. In Japan, due attention is warranted to the risk that Japan‑selling sentiment could spread via a sharp rise in interest rates and accelerated yen depreciation stemming from fiscal concerns. Global real GDP growth is projected at 3.2% in both 2026 and 2027.

The U.S. economy in 2025 maintained resilience even amid high uncertainty on geopolitical and trade fronts. This was driven by expanding domestic demand, with consumption and private capital expenditure driven primarily by AI‑related investment. The trend will continue in 2026, and the U.S. economy is likely to remain resilient. The inflation rate has continued to decline gradually, and the Fed is expected to implement two additional rate cuts in 2026. However, fading growth expectations for AI companies due to delays in monetization, as well as excessive intervention by the U.S. government in corporate and financial sectors, could lead to stock price corrections and an expansion of credit risk, thereby increasing the risk of recession. Real GDP growth in the U.S. is projected at 2.4% in 2026 and 1.9% in 2027.

The euro area economy in 2025 continued a moderate recovery. Although uncertainty related to U.S. trade policy increased at the beginning of the year, capital investment, mainly in Southern European countries, supported economic activity. In 2026, expansionary fiscal policies will be adopted, mainly in Germany, and the recovery of the euro area economy is expected to continue. The ECB is expected to keep its policy rate around 2% throughout 2026. In the UK, the economy has been stagnant due to fiscal tightening and an increase in unemployment. The BOE is expected to continue gradual rate cuts. Real GDP growth in the euro area is projected at 1.2% in 2026 and 1.3% in 2027. Real GDP growth in the UK is projected at 0.9% in 2026 and 1.2% in 2027.

China's economy faces stagnant investment and consumption. Corporate profit margins are declining amid intensifying competition, while sluggish real estate markets are impacting local government finances, leading to continued weak investment prospects. Although replacement incentive policies will continue through 2026, consumption growth will remain limited due to pull-forward effects and weak employment. Exports to ASEAN are growing, but increased anti-dumping measures against deflationary exports make sustained high growth unlikely. Under the 15th Five-Year Plan, where security is the top priority, local governments are trending toward lowering GDP targets. Real GDP growth is projected at 4.3% in 2026 and 4.0% in 2027.

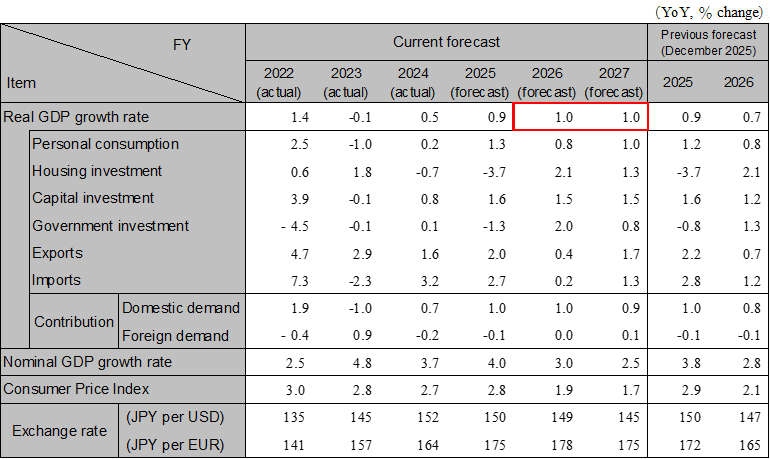

Japan's economy is expected to sustain its investment-led recovery, underpinned by robust corporate earnings and a labor shortage that has kept capital expenditure resilient. Consumption is projected to accelerate its recovery from mid-year, supported by continued wage improvements in the 2026 spring wage negotiations and the Takaichi administration's measures to ease household burdens. Although exports to China are slowing, the administration's focus on strategic investments is boosting momentum for enhancing industrial competitiveness. However, heightened market concerns over fiscal policy could trigger rising interest rates and yen depreciation, potentially causing a sharp stock market decline and leading to recession. Real GDP growth is projected at 1.0% in FY2026 (annualized 1.0%) and 1.0% in FY2027 (annualized 1.0%).

For India, the adverse impact on exports is expected to ease following a reduction in high U.S. tariff rates. Supported by tax cuts implemented since 2025 and increased infrastructure investment in the new fiscal year budget, relatively strong growth is expected to continue. The AI and digital sectors present both medium‑term opportunities and risks and warrant close attention. India’s growth is projected at 6.5% in FY2026 and 6.4% in FY2027. For the ASEAN‑5, broadly stable inflation and accommodative monetary policy are expected to support continued steady growth in the high‑4% range. While conditions vary by country and industry, caution is warranted regarding negative effects on local firms from deflationary exports from China. Real GDP growth for the ASEAN‑5 is projected at 4.7% in 2026 and 4.8% in 2027.

Note: Values for Japan differ from those shown in the table below on a fiscal-year basis because they are on a calendar-year basis. India’s figures are shown on a fiscal-year basis. ASEAN5 is comprised of Indonesia, Thailand, Malaysia, the Philippines, and Vietnam.

Source: Actual figures are from the IMF, forecasts are from the IMF (Brazil and Russia), and Hitachi Research Institute (others)

Note: The individual numbers and their sum may not match due to fractional processing.

Source: Cabinet Office, forecasts by Hitachi Research Institute

We provide you with the latest information on HRI‘s periodicals, such as our journal and economic forecasts, as well as reports, interviews, columns, and other information based on our research activities.

Hitachi Research Institute welcomes questions, consultations, and inquiries related to articles published in the "Hitachi Souken" Journal through our contact form.