Jun. 19, 2026

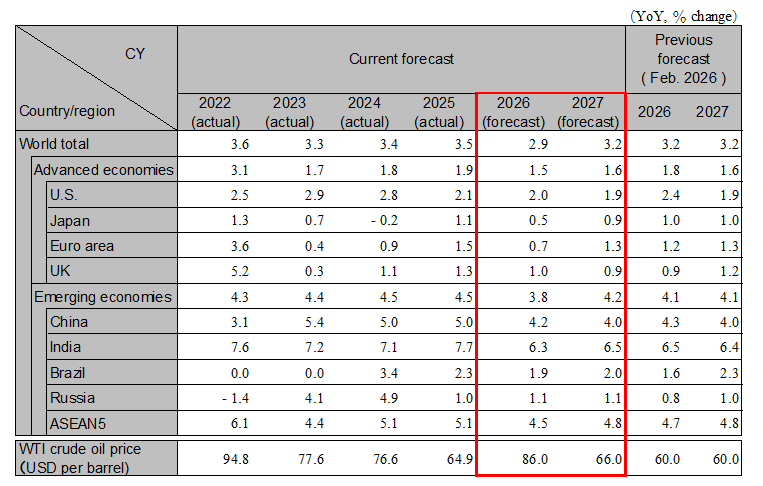

Global economic uncertainty is increasing amid the outbreak of war involving the U.S., Israel, and Iran. Robust AI-driven demand has so far helped avert a sharp economic downturn; however, going forward, disruptions in the logistics of crude oil and other resources and materials, along with rising prices, are expected to become more pronounced and weigh on global growth. Further escalation of Middle East instability could trigger global stagflation. Although AI remains a key growth driver, supply constraints such as power shortages and semiconductor bottlenecks, together with inflation-driven interest rate increases, could hinder its sustained expansion. Continued vigilance is also warranted regarding the risk of a sell-off in Japanese assets stemming from fiscal concerns. Global real GDP growth is projected at 2.9% in 2026 and 3.2% in 2027.

The U.S. economy continues to show resilient growth, supported by robust capital investment driven by strong AI-related demand. While investment-led expansion is expected to persist into 2026, elevated gasoline prices amid ongoing uncertainty in the Middle East are weighing on consumer sentiment, with private consumption likely to slow. In response to rising inflation, the Fed is expected to hold policy rates steady in 2026. There is also the risk that surging AI investment may outpace power and component supply, leading to investment bottlenecks, downward revisions to earnings expectations, equity market declines, and an economic slowdown. Real GDP growth in the U.S. is projected at 2.0% in 2026 and 1.9% in 2027.

The euro area economy is gradually slowing, as rising energy prices weigh on household and business sentiment. While increased defense spending will continue to support growth in 2026, the boost from AI investment remains limited. Ongoing uncertainty in the Middle East is expected to weigh on domestic demand. Amid inflation concerns, the ECB has shifted to rate hikes for the first time in three years and is expected to implement additional hikes in the second half of 2026. In the UK, inflation is also projected to accelerate in late 2026, leading to slower growth, with the BOE likely to follow suit and shift toward rate hikes. Real GDP growth in the euro area is projected at 0.7% in 2026 and 1.3% in 2027. Real GDP growth in the UK is projected at 1.0% in 2026 and 0.9% in 2027.

Although the Chinese economy is showing signs of recovery at present, strong growth is unlikely given that the government has lowered its growth target for 2026 and plans to keep fiscal spending—including infrastructure—at the previous year’s level. Persistent excessive competition in the manufacturing sector, particularly in the automotive industry, and rising costs due to the situation in the Middle East are squeezing corporate profits and curbing new investment. Consumption is expected to remain stagnant due to a decline in disposable income, the scaling back of replacement purchase incentives, and a sluggish real estate market. Exports are expected to remain robust, but there is a risk of sluggish growth if anti-dumping measures by ASEAN and Latin American countries increase or if economic slowdowns occur in various nations. Real GDP growth is projected at 4.2% in 2026 and 4.0% in 2027.

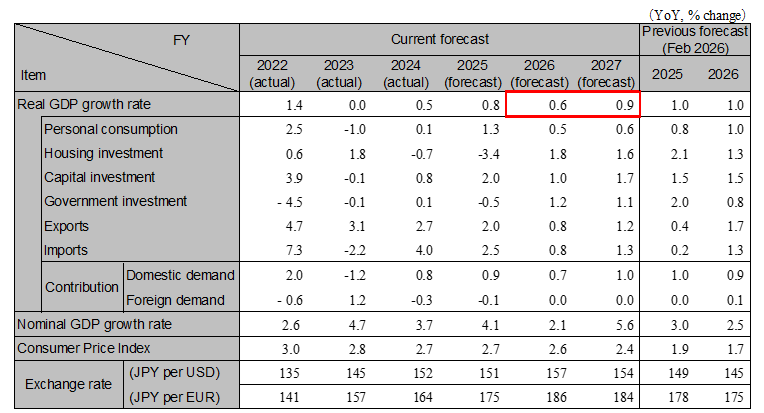

The Japanese economy continued a steady recovery through early spring; however, going forward, rising raw material prices are expected to weigh on growth. In particular, in the second half of FY2026, private consumption is expected to show signs of stagnation in response to a decline in real wages. While exports and capital investment will be supported by demand related to AI, and corporate profits are expected to expand steadily, the spillover effects to the overall economy will be limited. Close attention should be paid to risks originating from financial markets, such as a sharp decline in stock prices and a further rise in interest rates. Real GDP growth is projected at 0.5% in calendar 2026 (0.6% in fiscal year terms) and 0.9% in 2027 (0.9% in fiscal year terms).

India continues to see strong domestic demand-led growth, with FY2025 growth reaching 7.7%. However, the rupee remains under pressure amid concerns over a widening current account deficit driven by higher resource prices. Although resilient domestic demand is expected to sustain solid growth, rising inflationary pressure stemming from resource inflation and currency depreciation warrants close monitoring. India’s growth is projected at 6.3% in FY2026 and 6.5% in FY2027. For ASEAN5, attention should be paid to the risk of faster currency depreciation amid deteriorating fiscal conditions and weakening creditworthiness. ASEAN5 real GDP growth is forecast at 4.5% in 2026 and 4.8% in 2027.

Note: Values for Japan differ from those shown in the table below on a fiscal-year basis because they are on a calendar-year basis. India’s figures are shown on a fiscal-year basis. ASEAN5 is comprised of Indonesia, Thailand, Malaysia, the Philippines, and Vietnam.

Source: Actual figures are from the IMF, forecasts are from the IMF (Brazil and Russia), and Hitachi Research Institute

(others)

Note: The individual numbers and their sum may not match due to fractional processing.

Source: Cabinet Office, forecasts by Hitachi Research Institute

We provide you with the latest information on HRI‘s periodicals, such as our journal and economic forecasts, as well as reports, interviews, columns, and other information based on our research activities.

Hitachi Research Institute welcomes questions, consultations, and inquiries related to articles published in the "Hitachi Souken" Journal through our contact form.