The pursuit of energy transition—a shift in the energy supply and consumption structure from fossil fuels to renewable energy aimed at achieving carbon neutrality or decarbonization—was a dominant global trend following the Paris Agreement of 2015. At present, however, the confluence of global geopolitical shifts and rapid digitalization has rendered the landscape for energy transition complex and uncertain.

This transformation is rooted, first, in geopolitical and economic factors. The onset of the Russia-Ukraine war in 2022 led to the weaponization of energy, severe natural gas supply-demand imbalances, and soaring prices. In response, nations and regions have reaffirmed the critical importance of energy security and economic efficiency.

Furthermore, as of 2025, a pivotal technological undercurrent reshaping the energy market is the exponential advancement of digital technologies, particularly generative AI. While AI imposes significant burdens on energy systems through the immense power consumption of its foundational data centers (DCs), it also holds the potential to accelerate the energy transition itself through the development of new technologies.

This report seeks to project a future vision for the interplay between AI and energy in 2035, a future marked by heightened uncertainty. It also provides an outlook on the energy systems required to underpin the continued growth of AI and digitalization.

The accelerating evolution of AI technology can significantly contribute to climate action. For example, as power grids grow more complex with the large-scale integration of renewables, AI can enhance the precision of forecasts for variable renewable energy (VRE) sources like solar and wind, as well as for energy demand. By optimizing the supply-demand balance through energy storage systems and demand response, AI can help achieve the dual goals of expanding renewable energy capacity and ensuring grid stability. Furthermore, AI is expected to drive energy conservation by optimizing manufacturing processes and to accelerate the development of novel materials with high CO2 absorption efficiency and next-generation battery materials. Concurrently, AI is a key enabler for addressing a broad spectrum of societal issues, from labor shortages and improving healthcare quality to advancing urban functionalities.

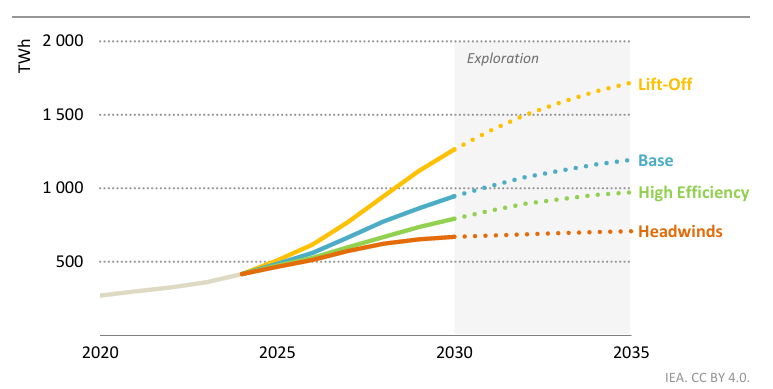

Conversely, the rapid growth and widespread adoption of AI introduce substantial risks to energy infrastructure. Current AI models’ training and inference require immense and sustained energy consumption to power vast computational resources in DCs. While conventional DCs were typically around the 10-megawatt (MW) scale, the demands of AI are driving a massive increase in size. The Stargate initiative, a plan for a super-scale DC announced by OpenAI in 2024, is projected to potentially reach the 5-gigawatt (GW) level. According to the International Energy Agency (IEA), this is equivalent to the power capacity of five million homes. In a report on AI and energy released in April 2025, the IEA predicts that global DC electricity consumption could surge from 415 terawatt-hours (TWh) in 2024 to 1,700 TWh by 2035 in the highest scenario*1 (Figure 1). The IEA notes that, although the total increase in global DC power demand is modest compared with the electrification of industry and transportation, the geographic concentration of DCs and the sheer scale of consumption at individual sites create localized demand surges. This places immense strain on transmission and distribution (T&D) infrastructure and heightens the risk of tightening power supply-demand balances.

At the same time, this could restrict the growth of the AI and DC industries themselves. In the U.S., Northern Virginia—the world's largest DC hub—is facing a situation where the expansion of T&D infrastructure is failing to keep pace with the increase in demand, resulting in a waiting period of up to seven years for new connections. Similarly, in Europe, a lack of grid capacity around Dublin, Ireland, has led to a de facto moratorium on new DC connections.

However, projecting AI-related electricity demand through 2035 is fraught with significant uncertainty. This uncertainty stems from several factors. First, it is uncertain whether the race to develop AI models based on the so-called "scaling law" will continue in the long term. Under the “scaling law,” it is assumed that the training performance of an AI model improves in a predictable manner depending on the number of model parameters (model size), the size of the training dataset, and the total amount of computation used for training. It is also uncertain how the trend of requiring more computation for higher-precision or more complex inference tasks (e.g., image/video generation, dialogue) will evolve.

Second, improvements in energy efficiency of hardware such as semiconductors and foundation models also have a significant impact on electricity demand. According to Epoch AI, an AI research institute, the energy efficiency of machine learning hardware improved by an average of approximately 40% per year from 2016 to 2024*2. In January 2025, moreover, DeepSeek-R1, a Chinese foundation model attracted global attention for its potential to achieve significantly higher energy efficiency in inference compared to previous models. However, it should be noted that these efficiency gains could be negated by the sheer growth in model size and the explosive proliferation of AI applications. Epoch AI also reports that the power required to train frontier AI models is doubling annually, far outpacing hardware efficiency improvements*3. Furthermore, the "Jevons Paradox" cannot be ignored: the possibility that falling training and inference costs will broaden AI's applications, thereby increasing overall usage and total energy consumption. The proliferation of generative AI for images and advanced robotics could trigger an explosion in societal AI use, driving up power consumption on a scale that overwhelms efficiency gains in both hardware and foundation models.

Source: IEA (2025), “Energy and AI,” p. 67. URL:https://iea.blob.core.windows.net/assets/34eac603-ecf1-464f-b813-2ecceb8f81c2/EnergyandAI.pdf

Figure 1: Global Data Center Energy Consumption Forecast (2020-2035, by Scenario)

For policymakers and corporations in the AI, digital, and energy sectors charting a course for the 2035 energy transition, a multifaceted perspective is essential. They must simultaneously maximize the "opportunities" presented by AI—accelerating the energy transition and solving broad societal challenges—while confronting the "challenge" of AI's own burgeoning energy consumption. To sustainably expand the benefits of AI while effectively managing its increasing energy consumption requires an integrated approach. This involves harmonizing technology development, infrastructure investment, policymaking and strategic guidance, and public consensus-building, all while navigating the complex interactions and trade-offs between digital and energy infrastructures.

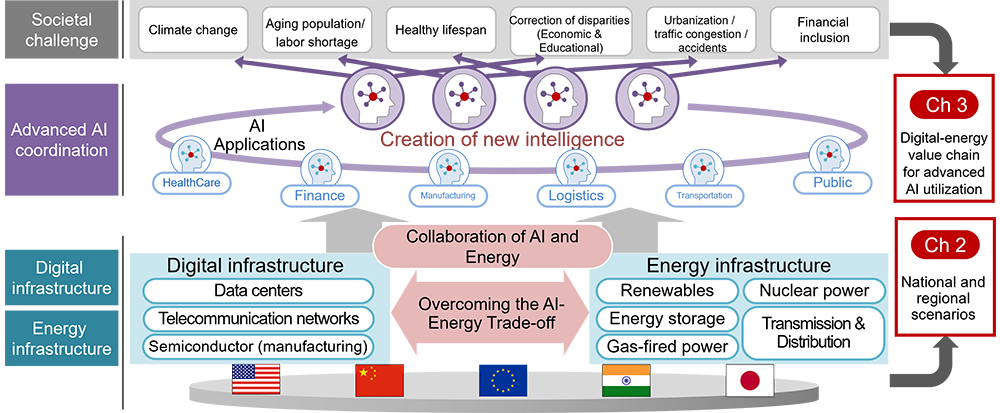

Figure 2 illustrates a vision for 2035 where AI and energy work together to realize a sustainable society, overcoming the trade-offs between digital and energy infrastructure by fully leveraging technology. The specific shape of this future vision will differ based on the unique energy infrastructure circumstances of each country and region. Therefore, Chapter 2 will provide an overview of global and key regional energy infrastructure scenarios for 2035. Meanwhile, the characteristics of AI model training and inference vary depending on the specific application within an industry, such as R&D in pharmaceuticals or operations and maintenance in manufacturing. Consequently, the digital and energy infrastructure needs of these industries also differ. Chapter 3 will therefore explore the future symbiotic value creation system (referred to as a "value chain" in this report) of digital and energy infrastructure that will support advanced AI applications in 2035. Finally, Chapter 4 will outline the challenges ahead in forming a new ecosystem where digital and energy infrastructures achieve true collaboration.

Figure 2: A Vision for 2035: The AI-Energy Symbiotic Ecosystem (HRI analysis)

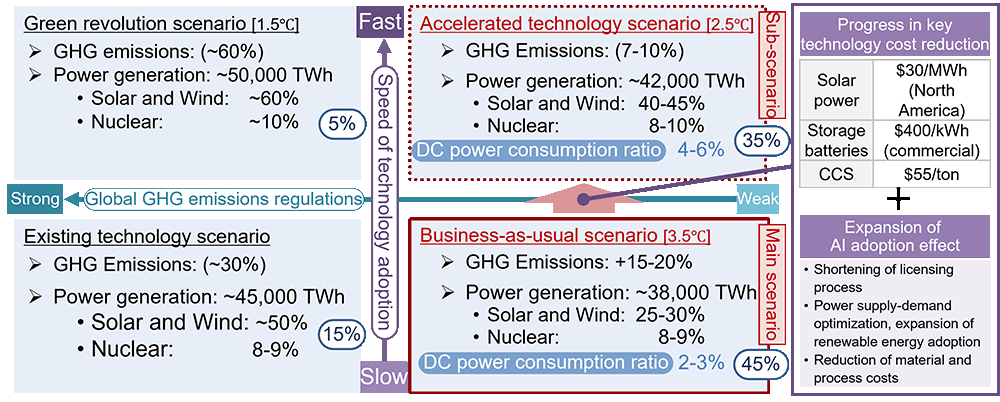

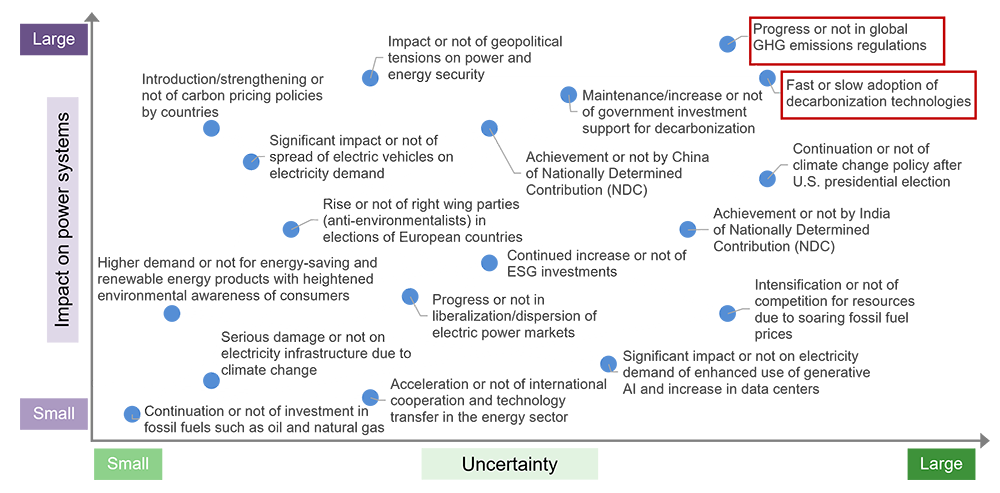

In examining energy scenarios for major countries and regions, HRI first conducted a scenario analysis to develop multiple global energy transition scenarios for 2035. Energy scenarios are shaped by a wide array of global economic, political, security, and technological drivers. Using generative AI to create an extensive list of drivers, HRI refined these determinants through internal examinations within HRI and discussions with experts in Japan and overseas. Two determinants were ultimately selected based on their outsized impact on the energy system and their high degree of uncertainty (see Figure 12 at the end of this report) : the stringency of international greenhouse gas (GHG) emission regulations, and the pace of energy-related technology adoption. The combination of these two determinants yielded four distinct global scenarios (Figure 3). The 29th session of the Conference of the Parties to the United Nations Framework Convention on Climate Change (COP29) in November 2024 highlighted the conflict between developed and developing nations. Subsequently, the second Trump administration, inaugurated in the U.S. in January 2025, signed an executive order to withdraw from the Paris Agreement. With U.S. funding for climate initiatives in developing countries unlikely for the foreseeable future, restoring international cooperation to strengthen GHG regulations for the 2050 carbon neutrality goal appears challenging. On the other hand, looking at trends in the development of energy-related technologies and their introduction, including their economic efficiency, we can see that while the costs of solar PV and battery storage continue to fall, recent inflation and rising interest rates have eroded project profitability. Furthermore, a U.S. tariff hike announced in 2025 and China's tightening export controls on rare earth elements have raised concerns about equipment cost inflation and material supply stability. Moreover, economic and technical hurdles also remain for the full-scale implementation of next-generation clean energy technologies like hydrogen. Accordingly, HRI designates the "Business-as-Usual" (BAU) Scenario—characterized by weak GHG regulations and a linear pace of technology adoption—as our main scenario. The "Accelerated Technology" Scenario—where technology adoption is fast-tracked by policy support and breakthroughs, despite weak GHG regulations—is considered the sub-scenario.

In the BAU Scenario, the slow progress on both GHG regulations and new technology adoption perpetuates a heavy reliance on fossil fuels across sectors like power generation and transportation. Under this scenario, the build-out of T&D infrastructure for AI data centers would be insufficient to meet demand, thereby constraining both power supply and the growth of AI DCs. In contrast, the Accelerated Technology Scenario sees rapid technological uptake despite lax GHG regulations. In addition to cost reduction in clean technologies such as solar and battery storage, the adoption of AI will result in a wide range of benefits, such as shortening the licensing process for T&D grids and power plants including small modular reactors (SMRs), and increasing the availability of renewables by optimizing power supply and demand.

The vision outlined in Section 1.2—one characterized by advanced AI utilization supported by a strengthened energy supply for digital infrastructure—could align with the Accelerated Technology Scenario. However, as will be discussed later, apart from trends in global GHG regulations and the speed of spreading a wide range of technologies, it is also necessary to consider the possibility of independent progress in the adoption of AI-related energy technologies due to national and regional industrial policies and private investment.

(Note) DC: Data Center. ‘~’ denotes an approximate value. Values in parentheses are negative. GHG emission reduction, power generation, and power supply configuration are estimated for each scenario based on IEA's World Energy Outlook 2024. Although power generation is the lowest in the BAU Scenario, overall GHG emissions will increase due to the increased GHG emissions from coal-fired power generation and the transportation sector.

Figure 3: Global Energy Transition Scenario for 2035 (HRI analysis)

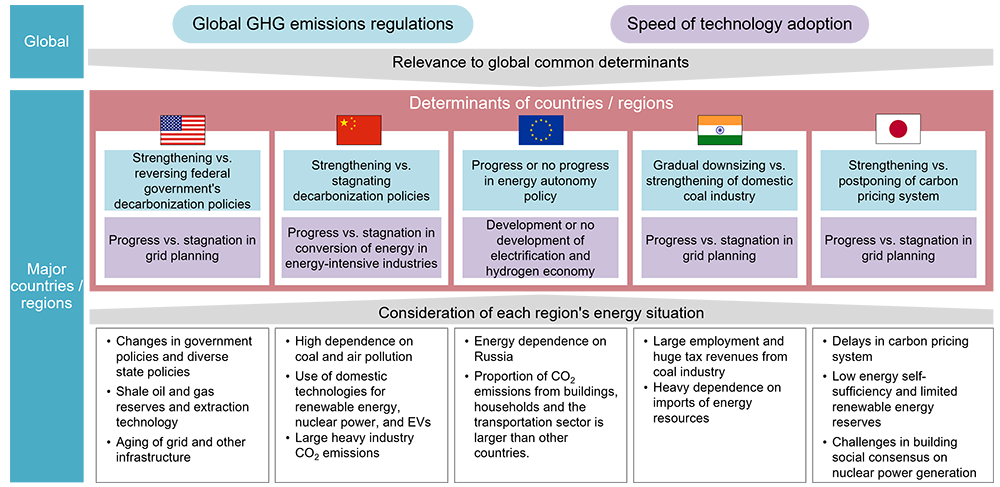

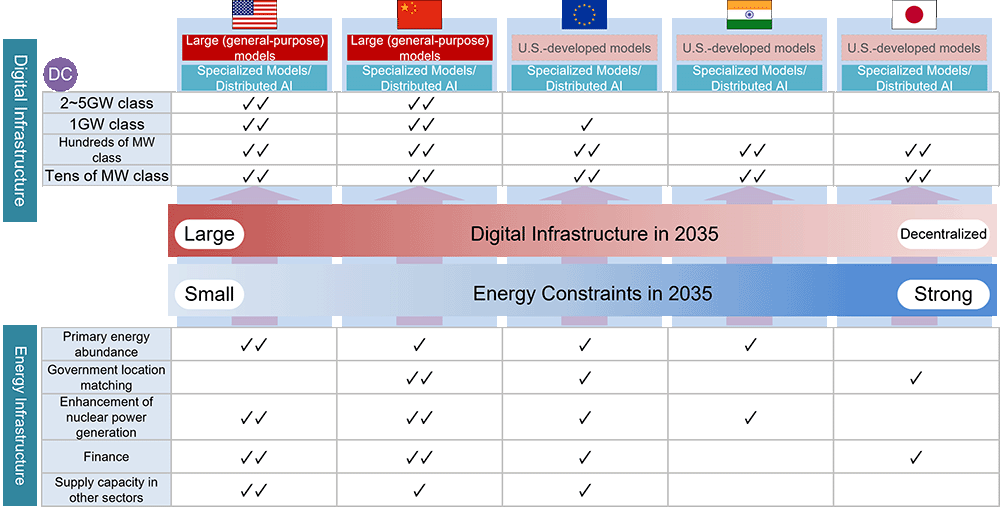

Country- and region-specific scenarios must reference the two global determinants while incorporating unique local energy determinants (Figure 4). Using the same methodology as the global analysis, two key determinants were selected for each region. For the U.S., they are the intensification or reversal of federal decarbonization policies, and the progress or stagnation of plans to expand and upgrade the T&D grid. For Europe, they are progress in the energy autonomy policy and development of electrification and a hydrogen economy. For Japan, the drivers are progress in strengthening the carbon pricing system and, similar to the U.S., the progress of its T&D grid expansion plan.

In the U.S., the second Trump administration, inaugurated in January 2025, issued an executive order to promote the use of oil, natural gas, and coal. The main scenario posits that federal decarbonization policy will remain stagnant long-term, but that T&D grid development, aimed at fostering industrial growth, will proceed regardless of the administration. Europe, after prioritizing environmental measures under its Green Deal policy since 2020, has recently shifted focus toward industrial competitiveness and innovation with its Clean Industrial Deal. However, high costs are forcing a review of hydrogen projects, raising concerns about achieving the 2030 targets for domestic hydrogen production and imports. The main scenario assumes that while energy autonomy policies will advance, the development of the broader electrification and hydrogen economy will be delayed. In Japan, the Seventh Strategic Energy Plan was approved by the Cabinet in February 2025, scheduling the introduction of a mandatory emissions trading system (GX-ETS) within the GX League framework. The main scenario assumes that the carbon pricing system will continue to be strengthened, but that the development of the T&D grid will be delayed.

Figure 4: Determinants of Scenarios for Major Countries and Regions (HRI analysis)

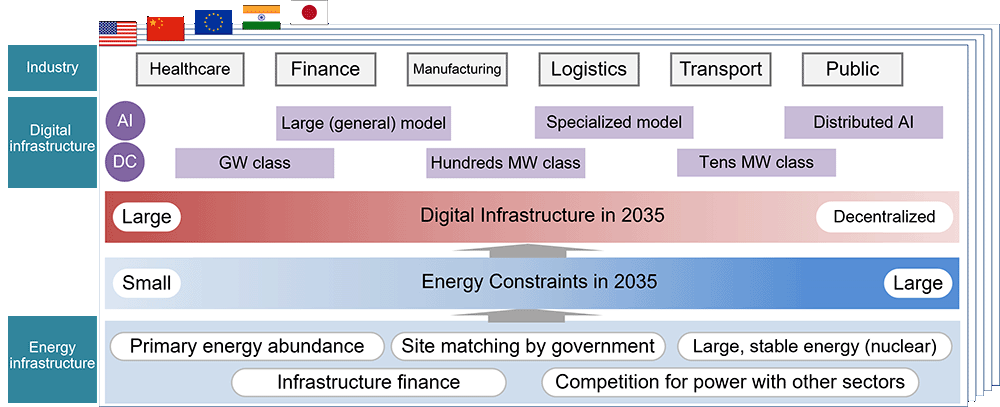

The deployment model for AI digital infrastructure in 2035 will be heavily influenced by the magnitude of each region's "energy constraints"—a term encompassing energy supply capacity and grid limitations (Figure 5). Specifically, the degree of energy supply constraints on digital infrastructure is determined by a combination of factors, including domestic energy resource endowment, matching of digital infrastructure and energy infrastructure by governments through siting policies and guidance, the feasibility of new, large-scale, stable power sources like nuclear (including SMRs), the financing environment for digital infrastructure and energy infrastructure, and the competition for T&D grids and power capacity among different sectors. Regions with relatively low energy constraints will be able to construct massive, multi-GW-scale DCs. In contrast, regions with high constraints will find large-scale development challenging, likely leading to a focus on smaller, distributed DCs in the tens-of-MW range.

(Note) GW: Gigawatt, MW: Megawatt

Figure 5: Selection of Digital Infrastructure and Energy Infrastructure by Country and Region (HRI analysis)

Figure 6 provides examples of digital infrastructure options based on regional energy constraints in 2035. The U.S. possesses abundant domestic resources, including natural gas, in addition to renewables. To minimize the impact of T&D grid development delays, there is a growing trend of on-site generation, where gas-fired power plants are co-located with DCs, leveraging the nation's extensive natural gas pipeline network. Furthermore, new nuclear development, including SMRs, is advancing, supported by direct investment and Power Purchase Agreements (PPAs) from Big Tech companies like Microsoft and Google. Consequently, even under the main scenario where federal decarbonization policy stalls (as described in 2.2), private-sector investment and development of specific technologies like SMRs will continue to accelerate, driven by AI demand and the imperative to bolster industrial competitiveness. This results in relatively low energy constraints, enabling the construction of large-scale digital infrastructure. Ultimately, this allows for the development and operation of large-scale foundation models in super-giant DCs (2+ GW), in addition to specialized and distributed AI in small- to medium-sized DCs.

Japan, on the other hand, has scarce domestic energy resources, and building new nuclear power plants remains difficult under current conditions, resulting in significant energy constraints. Therefore, under any scenario, the hurdle for constructing GW-scale DCs is high. For Japan, developing and utilizing specialized models and distributed AI via small- and medium-sized DCs emerges as the more pragmatic path.

Figure 6: Digital Infrastructure Options based on Energy Constraints by Country and Region in 2035 (HRI analysis)

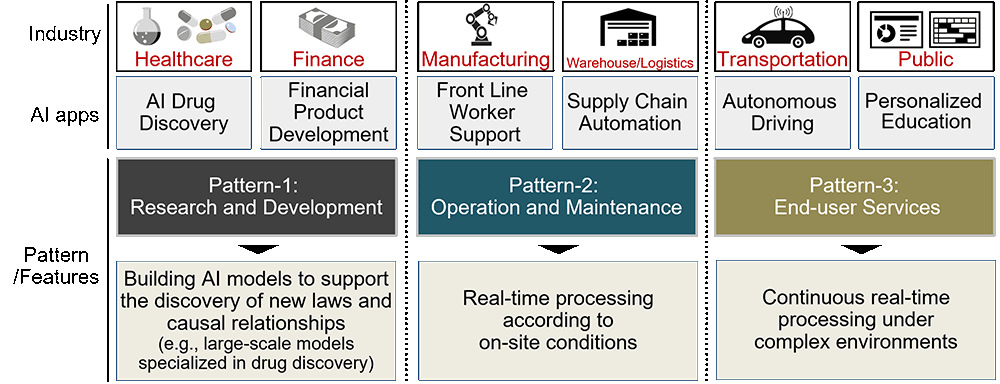

The nature of AI model training and inference varies significantly depending on the application and industry. Consequently, constructing an optimal digital-energy value chain tailored to the specific characteristics of the AI workload is imperative. HRI considered the value chains of digital and energy infrastructure supporting AI applications across the following three areas (Figure 7).

Figure 7: Patterns and Characteristics of AI Utilization by Industry and Application (HRI analysis)

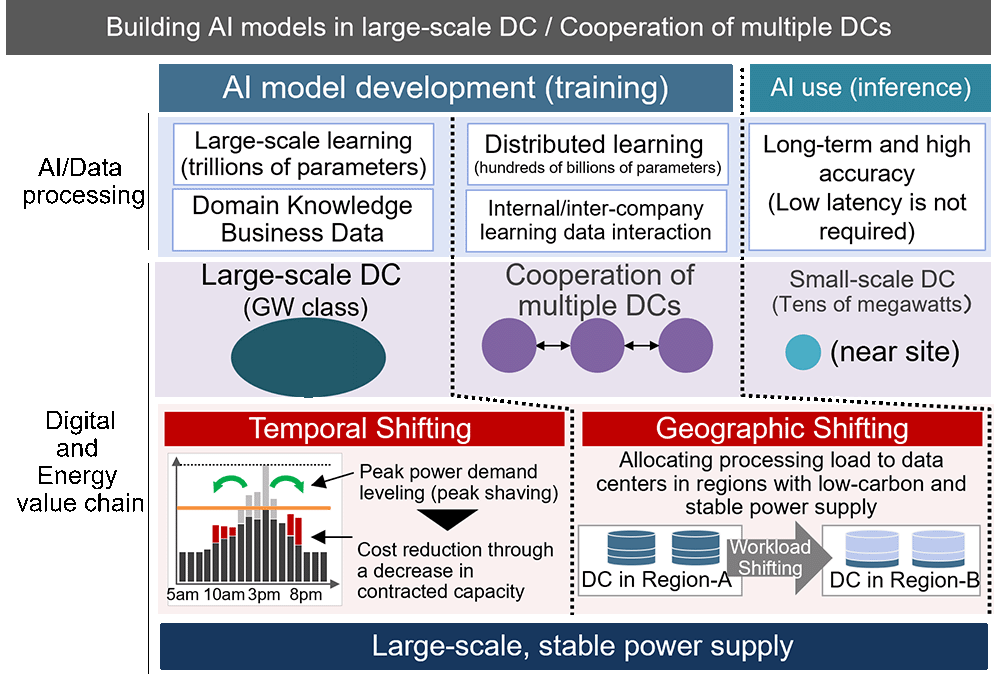

AI models for research and development are expected to be large-scale (hundreds of billions of parameters or more), with enormous computational requirements for training. This suggests that training will be processed centrally at large, GW-scale DCs. While this processing incurs massive power demand, the training itself does not require high-real-time performance. This allows for temporal load shifting—distributing the AI processing load by scheduling training tasks during off-peak hours, such as at night or when renewable energy supply is abundant. This practice enables the leveling of DC power demand and peak shaving. However, given power supply and other constraints, not all regions or companies can build models on large-scale DCs. An alternative approach is federated or distributed model training, where multiple DCs collaborate. In such cases, geographic load distribution among DCs in different locations makes it possible to maximize the use of regional energy resources, thereby enabling more sophisticated and efficient processes in fields like drug discovery and financial product development.

Figure 8: Value Chain for Research & Development Applications (HRI analysis)

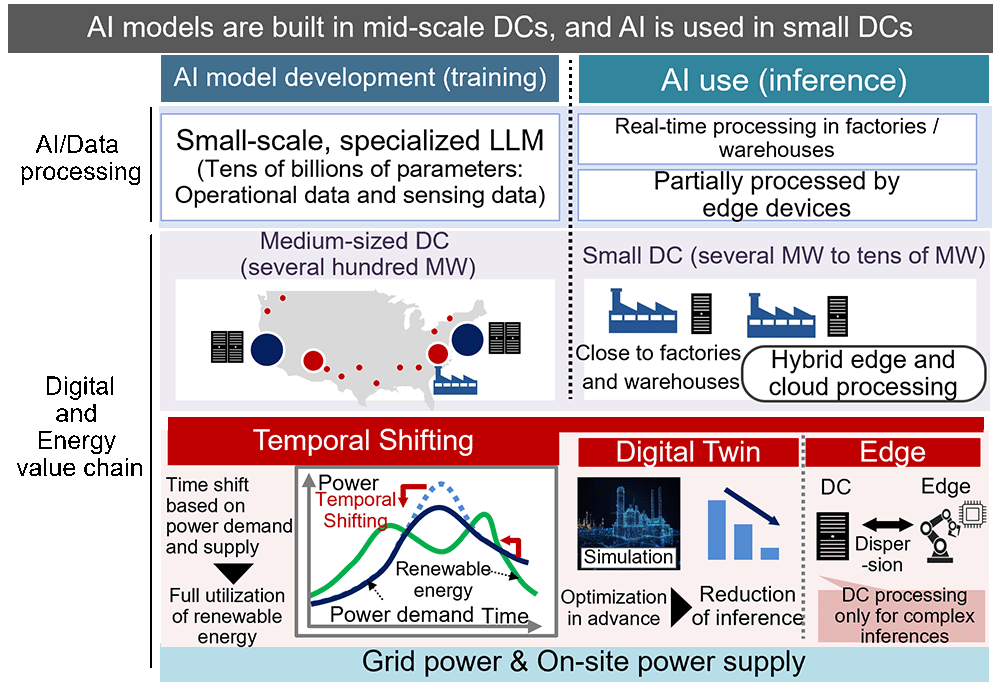

In manufacturing and logistics, operations and maintenance applications typically require specialized, smaller-scale AI models (tens of billions of parameters) trained on industry- specific or company-specific data. Crucially, the AI utilization phase demands real-time processing capable of second-by-second decision-making and control with on-site conditions. For these use cases, model training is performed at mid-sized DCs (hundreds of MW), while low-latency inference is achieved by deploying small-scale DCs in close proximity to the operational site, such as a factory. As the use of AI and robotics in factories increases, so does the load and power demand on these DCs. A critical challenge, therefore, is ensuring low-carbon operations through renewable energy to meet industrial decarbonization goals. Where processing times are flexible (e.g., production planning and forecasting), temporal load shifting becomes a viable option, aligning computational workloads with fluctuating renewable energy supplies. Furthermore, digital twins can be used to optimize production processes in advance, reducing the need for repeated inference. Edge computing can also be leveraged to execute simpler tasks on local devices (e.g., factory robots), reserving DC resources for complex computations. This hierarchical processing model helps suppress energy consumption peaks caused by processing concentration at the DC.

(Note: LLM: Large Language Model)

Figure 9: Value Chain for Operations & Maintenance Applications (HRI analysis)

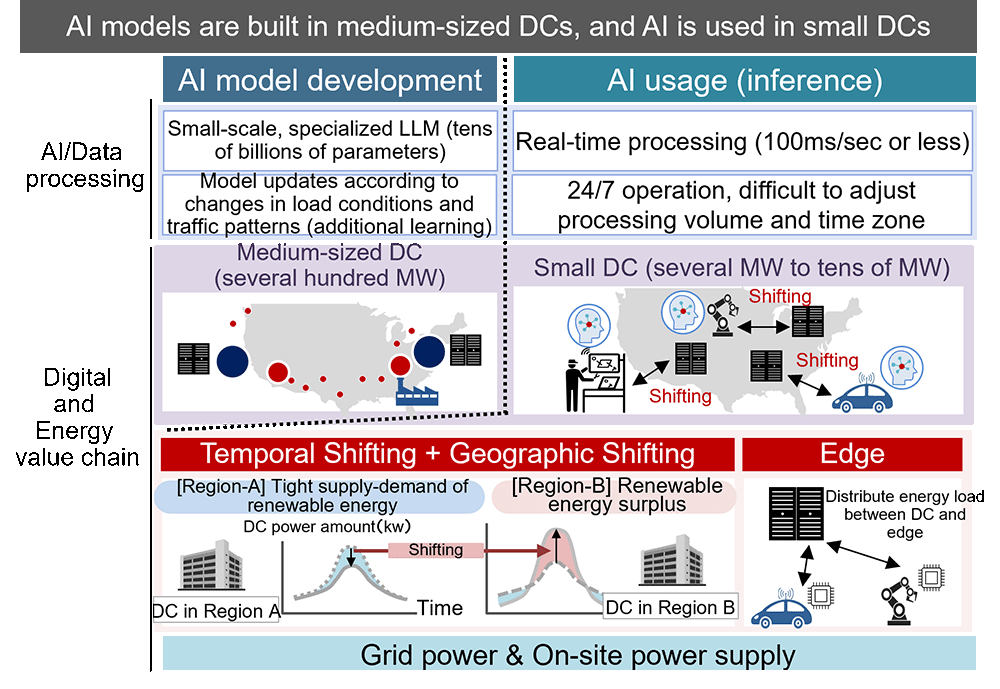

In the end-user services, applications must respond instantly to real-world environment changes. This requires constant real-time processing under complex conditions, in addition to the use of specialized AI models. For example, autonomous vehicles must continuously make judgments and control actions by instantly processing a multitude of variables—pedestrians, signals, other vehicles, weather, and road conditions. Training advanced AI models (tens of billions of parameters) that enable this level of judgment is expected to require mid-sized DCs (hundreds of MW). During the AI utilization phase, low-latency and efficient inference can be achieved by deploying small, distributed DCs in urban areas where many users access the service simultaneously. In scenarios where devices like autonomous vehicles are constantly generating and processing data, requiring continuous AI inference, the load on specific DCs can become immense. Therefore, in addition to temporal load shifting, a combination of geographic load balancing across multiple DCs and load distribution between DCs and the edge (devices) is employed. This enables end-users and service providers to have a seamless and safe experience, free from concerns about communication latency.

As illustrated, realizing advanced AI applications to solve societal challenges requires the development of optimal and resilient digital-energy value chains tailored to the unique characteristics and patterns of each application.

Figure 10: Value Chain for End-User Service Applications (HRI analysis)

The global energy transition scenarios for 2035 and the digital-energy value chains that will support advanced AI applications have been explained in the above sections. In this section, we provide an outlook on the evolving relationship between the digital and energy sectors and envisions a future of symbiotic cooperation to achieve efficient resource utilization and solve critical societal problems.

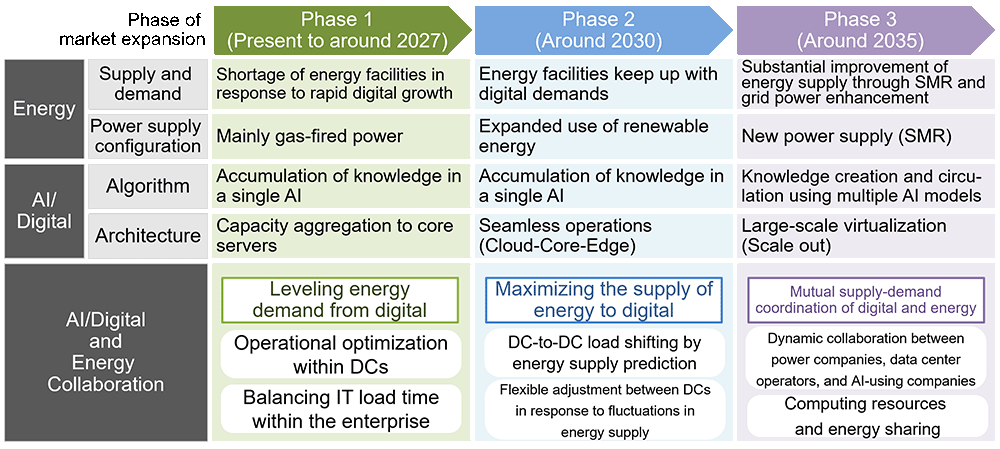

The challenges and solutions for realizing advanced AI will evolve in phases according to the supply-demand dynamics of energy for the AI/digital sectors. As shown in Figure 11, Phase 1 (Present to around 2027) is characterized by an energy supply deficit relative to the rapid growth in AI/digital demand. In this constrained environment, the primary challenge is to level energy demand from digital, as computational processes must operate within limited energy envelopes. This requires solutions like operational optimization within DCs and temporal shifting of IT workloads within the enterprise. In phase 2, energy supply capacity will begin to catch up with digital demand by the expansions of new renewable energy facilities and grid, though it cannot fully meet the demand. At this stage, maximizing energy delivery to the digital sector will be required through demands dynamic adjustments, such as flexible load shifting between DCs based on energy supply forecasts or moving workloads from DCs in energy-strained regions to those with a surplus. In Phase 3, significant energy supply enhancements from sources like SMRs and a reinforced grid will be sufficient to meet digital demand. Advances in AI technology and next-generation communication networks will enable mutual supply-demand orchestration between the digital and energy sectors. While dynamic coordination among power companies, DC operators, and AI users is expected, it also presents new challenges that massive datasets between AI models operating across different domains could cause intensive, short-duration computational loads on DCs. In such scenarios, the risks of sudden computational load spikes and communication latency become critical so flexible load management will be required through sharing computational resources among DC operators and AI users and implementing task prioritization. This allows for the dynamic adjustment of where and when high-intensity loads are processed. Ultimately, this advanced orchestration will enable specialized AI models from different industries and applications to collaborate in real-time, jointly tackling complex tasks and this is expected to make significant contributions to solving multifaceted societal challenges, including climate change and disaster response.

Figure 11: Future Vision of Cross-Industry AI Collaboration (HRI analysis)

AI and digital technology development has accelerated continuously, and the energy policy landscape is in constant flux. Based on the research on technology and policy trends in each region, HRI will consider challenges arising from this evolving relationship and solutions required to address the challenges.

Figure 12: Determinants of Global Energy Transition Scenarios (HRI analysis)

Nobumitsu Aiki

Senior Researcher, Policy and Environment Research Group, 1st Research Department, Hitachi Research Institute

He drives the conceptualization of next-generation infrastructure for a sustainable future and its corporate strategy design, with AI, digital technology, and energy at the core.

His current work centers on implementation strategies for 'AI for Energy & Energy for AI,' carbon neutrality, and the circular economy.

Prior to his current role, which he assumed in 2020, his career at Hitachi, Ltd., included international business development for railway control systems.

Shuntaro Ishii

Associate Senior Researcher, Global Business Strategy Group, 2nd Research Department, Hitachi Research Institute

He is engaged in the design and execution support of business and regional strategies in sustainability, AI and digital areas. His recent research work includes exploring the interrelationship between AI and energy, as well as the quantification and assessment of social impact.

Prior to his current role, his career at Hitachi, Ltd. included the sales of autonomous driving technology and advanced driver-assistance systems (AD/ADAS) in automotive business division.

Author’s Introduction

Nobumitsu Aiki

Senior Researcher,

Policy and Environment Research Group,

1st Research Department

Shuntaro Ishii

Associate Senior Researcher,

Global Business Strategy Group,

2nd Research Department

Energy Transition in New Dynamics of Geopolitics and AI Evolution

We provide you with the latest information on HRI‘s periodicals, such as our journal and economic forecasts, as well as reports, interviews, columns, and other information based on our research activities.

Hitachi Research Institute welcomes questions, consultations, and inquiries related to articles published in the "Hitachi Souken" Journal through our contact form.