![]()

Latest economic forecasts for Japan, the U.S., Europe, and China, etc

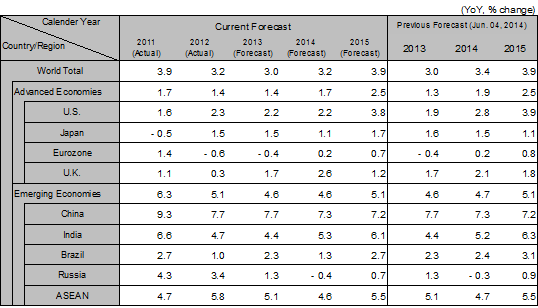

The growth rate of the global economy is expected to increase from 3.0% in 2013 to 3.2% in 2014 and 3.9% in 2015, mainly due to the accelerating growth of the Japanese and American economies and the Chinese economy's steady 7% growth level, despite risk that the deteriorating relationship between the EU and Russia over the Ukraine situation will return the European economy to recession.

In the U.S., the trend of rising employment has strengthened, household debt adjustment is nearly complete, and the recovery of personal consumption and housing investment is becoming more robust. The FRB will end QE3 (third round of quantitative easing) in its October 29 meeting; however, the zero interest rate policy will be maintained until the middle of 2015 to fiscally support the economy. Consequently, the U.S. economy's growth rate is expected to reach 2.2% in 2014 and accelerate beyond the 2.2% potential growth rate to 3.8% in 2015.

The Eurozone is on the brink of deflation due in part to the fall in exports to Russia in addition to each country's fiscal austerity policy. In particular, Italy has fallen into its third recession since 2008, and the prolonged economic stagnation continues in other southern European countries. The ECB is highly likely to move to additional monetary easing including QE (quantitative easing) within 2014 to fiscally support the economy. Growth rates are expected to be barely positive at 0.2% and 0.7% for 2014 and 2015, respectively, and resilience is weak.

In China, the effects of economic-stimulus measures consisting mainly of investment implemented in April have run out, housing prices have also been trending toward a fall for three consecutive months since May, and signs of deceleration in the economy are apparent. The government must continue with difficult maneuvering to maintain the targeted 7% level growth while controlling problems in the Chinese economy such as excessive equipment, inventory, and expansion of credit. The growth rate is forecast to be 7.3% in 2014 and 7.2% in 2015, and the 7% level of growth is expected to remain steady due to continuous support by policies including partial relaxation of housing market control measures, small scale economic-stimulus measures, and a policy of monetary easing, etc. However, risks such as a sharp decrease in exports from the deterioration of the European economy still remain.

Among emerging countries, India is showing signs of recovery in both consumption and among the Index of Industrial Production under the Modi administration, which is advocating proactive economic policies including the promotion of foreign investment. The most recent (April-June period) economic growth rate increased to the 5% level. The new administration plans to focus on restoring fiscal health, which has been a longstanding problem, as well as infrastructure development, and the growth rate is expected to gradually increase from 4.4% in 2013 to 5.8% in 2014 and 6.1% in 2015.

The future global economy faces two large risks. The first is the Ukraine risk: if 20,000 Russian troops invade eastern Ukraine, the European economy will once again fall into recession due to a deterioration of the economic relationship with Russia. The second risk is a sharp credit crunch in China: if a housing price drop quickly shrinks the inflated credit balance, China's growth rate will dip below 7%. If either risk develops, the impact will spread to the entire global economy, and there is a possibility that both 2014 and 2015 growth rates will fall below that of 2013.

The Japanese economy experienced significant negative growth and recorded an annualized growth rate of -7.1% on a quarter-on-quarter basis in the most recent April-June period, due to the drop from the backlash following the consumption tax rate increase. Even after the start of summer, unseasonable weather caused the recovery of personal consumption to lack strength. On the other hand, the ratio of active job openings to applicants for July increased to its highest level following the burst of the bubble economy, and employment continues to improve while capital investment is also on the way to recovery mainly due to replacement demand. Partly due to the early intensive execution of public works, growth will accelerate in the second half of the 2014 fiscal year, and the growth rate is forecast to be 0.6% in the 2014 fiscal year and 1.6% in the 2015 fiscal year. Increases in wages and commodity prices have nearly stabilized, and the 2% inflation target for 2015 set by Governor Kuroda of the Bank of Japan is achievable.

Based on the assumption that 1 trillion yen of economic-stimulus measures such as investment tax reduction and public investment will be executed along with a consumption tax increase (from the current 8% to 10%) in October 2015, if the economic recovery continues in the 2015 fiscal year, the deflationary gap that is estimated by the Cabinet Office at -2.2% in relation to potential GDP in the April-June period of 2014 is expected to be overcome in the 2015 fiscal year.

Note: Since the figures above are based on the calendar year, the figures for Japan are different from the fiscal-year based figures in the table below.

Source: IMF. Forecast by Hitachi Research Institute

Source: System of National Accounts, etc. Forecast by Hitachi Research Institute.