![]()

Latest economic forecasts for Japan, the U.S., Europe, and China, etc

The global economy is recovering, powered by fast U.S. recovery and China’s stable growth, but risk of a surge in COVID-19 infections lingers

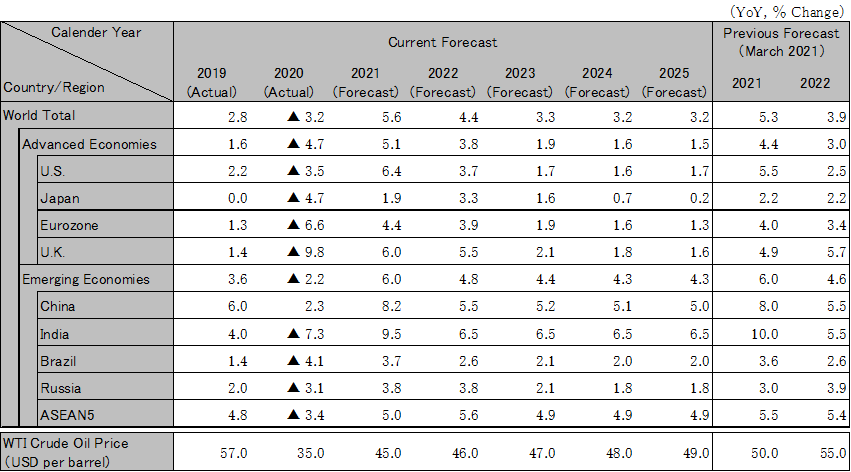

New infections are on the decline. Progress in vaccinations has been made mainly in the U.S. and Europe. The global economy is projected to grow from 2021 to 2022, led by the U.S., which is on a fast recovery track thanks to a large-scale economic stimulus package. China is expected to continue its stable expansion, while Europe will likely start its recovery in the second half of 2021. The projected global GDP growth rate is 5.6% for 2021, and 4.4% for 2022. However, in emerging countries, the spread of vaccines is expected to take place from the second half of 2022 to the first half of 2023. India faces the risk of an economic downturn mainly due to a resurgence of infections. Japan will likely see an accelerated inoculation pace from this summer onward. The greatest risk in 2021 is a global resurgence of infections caused by COVID-19 variants.

The Biden administration announced a large-scale economic stimulus package totaling approximately $6 trillion. Vaccinations also made rapid progress, and the U.S. economy took off smoothly in early 2021. The economy, mainly in service consumption, will likely remain firm in the second half of 2021 as well. It is projected that from 2022, infrastructure investment and family support measures will further boost fixed investment and consumption, driving the global economic recovery. Although the core inflation rate in 2021 is expected to temporarily exceed the 2% target due to tight supply and demand, the Federal Reserve will likely not react to it. Tapering is to start in 2022 and interest rate hikes will presumably come in late 2023. Real GDP growth rate projections are 6.4% in 2021, and 3.7% in 2022.

The Eurozone economy showed negative growth in early 2021 due to the extension of lockdown measures. Countries are recovering at varying speeds due to the differences in the status of infections and the magnitude of impact on each industry. However, economic recovery is expected to pick up speed from the latter half of 2021 due to (1) the spread of vaccines, (2) provision of recovery funds, and (3) recovery of economies outside the region, such as the U.S. and the UK. Real GDP growth rate forecasts for the Eurozone are 4.4% in 2021, and 3.9% in 2022. Note that in the 2021 German federal election scheduled for September, it is very likely that the Green party becomes part of the next government. The UK economy will likely recover at an accelerated pace in 2021 thanks to the relatively prompt progress of vaccinations. The real GDP growth rate for the UK is projected to be 6.0% in 2021, and 5.5% in 2022.

In the January-March quarter of 2021, the economy grew at a high rate of 18.3%, a reactionary increase from the previous year. However, quarter-on-quarter growth was actually muted at 0.6%, reflecting an equable recovery. Exports, mainly of pharmaceuticals and IT equipment, increased, supported by growth in demand worldwide, while investments in the manufacturing sector recovered as well. Consumption also recovered as employment and income conditions improved. Ahead of the Communist Party Congress in 2022, the country’s top leaders are expected to focus on maintaining the stability of the economy and the financial system, rather than pursuing excessive consumption stimulus measures and a rapid tightening of monetary policy. Real GDP growth rate projections are 8.2% in 2021, and 5.5% in 2022. Current risks include worsening international relations mainly with the U.S., Europe and India, and aggravating debt problems among domestic companies due to reduced financial assistance.

In India, the rapid surge in infections since late March 2021 is now coming down. The real GDP growth rate for FY2021 is expected to be 9.5% due to stagnancy early in the year despite showing a reaction to the slump in FY2020 and being backed by fiscal stimulus measures. There is still the risk of a resurgence in infections primarily caused by variants in connection with the relaxation of restrictions on economic activities. The pace of recovery among ASEAN countries will likely continue to vary. We see the need to pay attention to the risk of stagnation in economic activities due to a rise in the number of new infections even in Vietnam, where domestic and foreign demand is strong, and in Malaysia, where the economy may be driven by growth in exports.

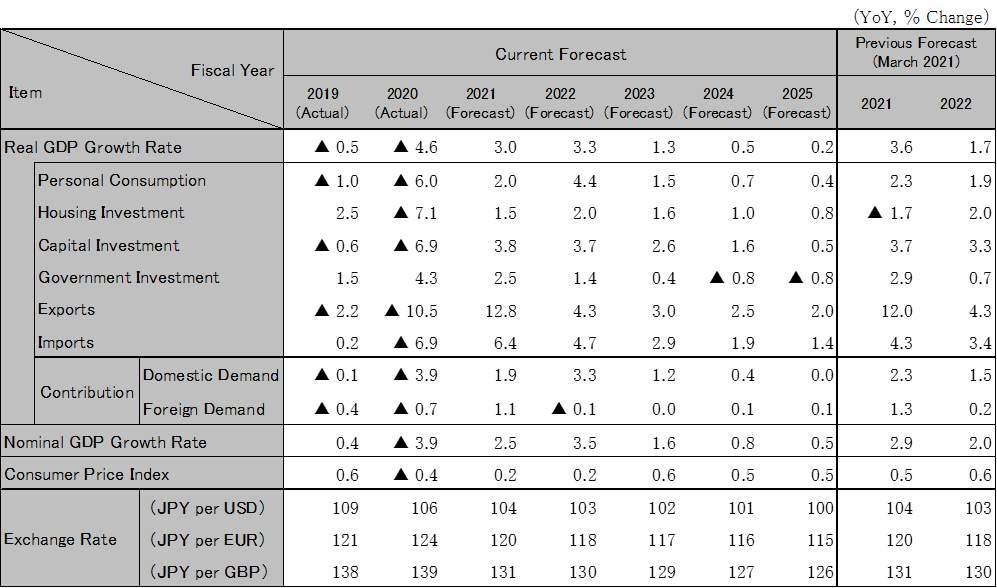

In the first half of 2021, consumption was sluggish and economic recovery was delayed mainly in the service industry because of the declaration of a state of emergency and the delay in the deployment of vaccines. On the other hand, growth in exports, mainly to China, supported a recovery in the production of production machinery and electronic components and devices. Capital investment is expected to recover, mainly in the manufacturing sector. Domestic demand will likely turn upward in line with an increase in public works projects supported by the third supplementary budget and a higher national resilience budget. In the second half of FY2021, demand for services, such as food and drink services, lodging, entertainment and public transportation, is expected to recover following progress in vaccinations and the lifting of restrictions on activities. Real GDP growth rate projections are 3.0% in 2021, and 3.3% in 2022. As potential growth rate will likely continue to decline, sustainable economic recovery will be crucial through the steady implementation of growth strategies and accelerated investments in green infrastructure and digital fields.

Note: The figures above are calendar-year based. Accordingly, the figures of Japan are different from the fiscal-year based figures in the table below.

Source: IMF. Forecast by Hitachi Research Institute.

Source: Japan Cabinet Office, etc. Forecast by Hitachi Research Institute.