![]()

Latest economic forecasts for Japan, the U.S., Europe, and China, etc

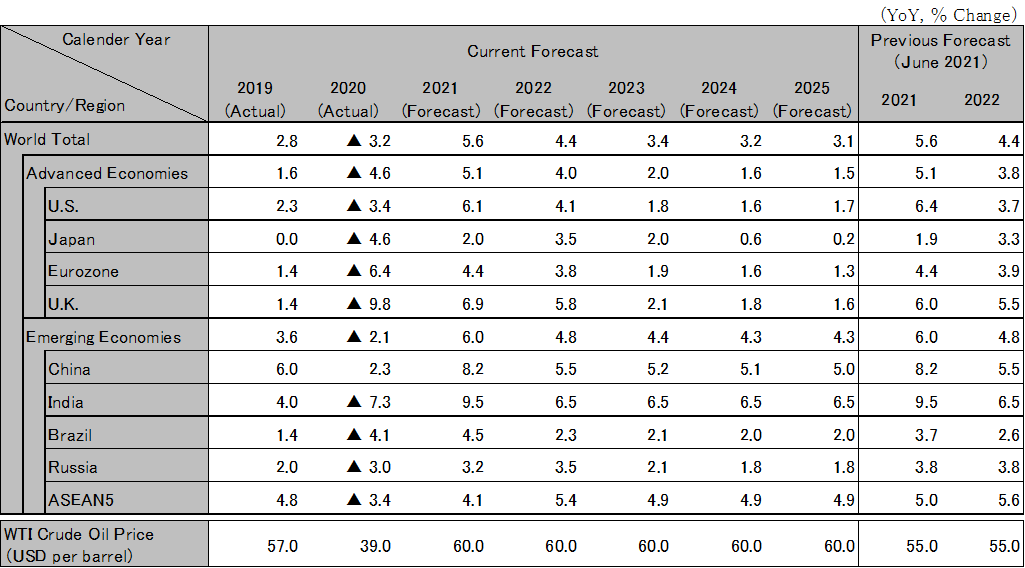

The global economy is expected to make an autonomous recovery toward stable growth in 2022 despite the lingering uncertainties over COVID-19 variants

Although new infections have been on the rise again since July due to variants, the impact on the economy is limited as developed countries that have made progress in vaccinations, such as the UK, ease restrictions on activities. On the other hand, ASEAN and other emerging economies are stagnant. In 2022, it is likely that progress will be made in the development and approval of effective curative drugs on top of vaccinations also in the developing countries. While the threat of variants will remain, the impact on economic activity is expected to be local. In 2021, an economic recovery will likely be achieved mainly in developed countries thanks to policy effects before shifting to a stable recovery phase that includes emerging countries in 2022. The projected global GDP growth rate is 5.6% for 2021, and 4.4% for 2022.

The U.S. economy is expected to remain strong in 2021 and 2022. Despite the spread of infections caused by the Delta variant, no restrictions are imposed on economic activities, limiting the impact of infections on the economy. The Biden administration is expected to pass additional economic stimulus measures totaling $4 trillion before the year-end. Anticipating that those economic measures will take effect in 2022, fixed investment and spending will likely drive an economic recovery. While the core inflation rate for 2021 exceeds the 2% target due to tightening of the demand-supply balance of goods, it is an acceptable level for the Federal Reserve. Tapering will likely begin in late 2021, and interest rates are to be raised in mid-2023. Real GDP growth rate projections are 6.1% in 2021, and 4.1% in 2022.

The Eurozone economy is expected to continue showing high growth in 2021 and 2022. Conditions in the service sector, where recovery had been lagging, have been improving thanks to the progress in vaccinations from May onward along with the easing of restrictions on activities. People have been returning to the streets in major countries. Although the prolonged shortage of semiconductors has caused production to stagnate in the manufacturing industry in Germany and other countries, the stagnation will likely be eliminated in 2022. It is projected that the rising trend in the inflation rate will calm down as service prices are stabilized. Real GDP growth rate projections for the Eurozone are 4.4% in 2021, and 3.8% in 2022. The UK avoided reimposing behavioral restrictions even after the spread of infections caused by the Delta variant. The UK economy is expected to recover in 2021 and 2022, led by personal consumption. The real GDP growth rate for the UK is projected to be 6.9% in 2021, and 5.8% in 2022.

The Chinese economy has moved from a post-COVID rapid recovery phase to a stable expansion phase. The economy maintains an expansion mode despite a slight slowdown in economic activity up to the summer of 2021 partly due to the impact of natural disasters. Consumption also continues to recover. Ahead of the Communist Party Congress in 2022, the country’s top leaders are expected to focus on operating measures to avoid instability of the economy and suppress dissatisfaction with the disparity among people. It is likely that the government will pursue financial easing as needed to support medium and small-sized businesses and promote infrastructure investment in order to prevent the economy from stalling while maintaining the measures to keep the real estate market from overheating. Real GDP growth rate projections are 8.2% in 2021, and 5.5% in 2022.

In India, the rapid surge in infections has been contained for the most part. Although the economy was stagnant in early FY2021, the real GDP growth rate is expected to recover to 9.5% in reaction to the slump in FY2020 and the effects of fiscal stimulus measures. The risk of new waves of variant infections caused by the delay in vaccinations remains, but the government will likely suppress the impact on the economy by implementing localized activity restrictions. Although the number of new infections in ASEAN countries increased in summer, infections are projected to wind down due to the effects of restrictions on activities from autumn onward. Domestic demand is expected to make an autonomous recovery by the latter half of 2022 supported by the spread of vaccines. The real GDP growth rate of ASEAN5 is projected to be 4.1% in 2021, and 5.4% in 2022.

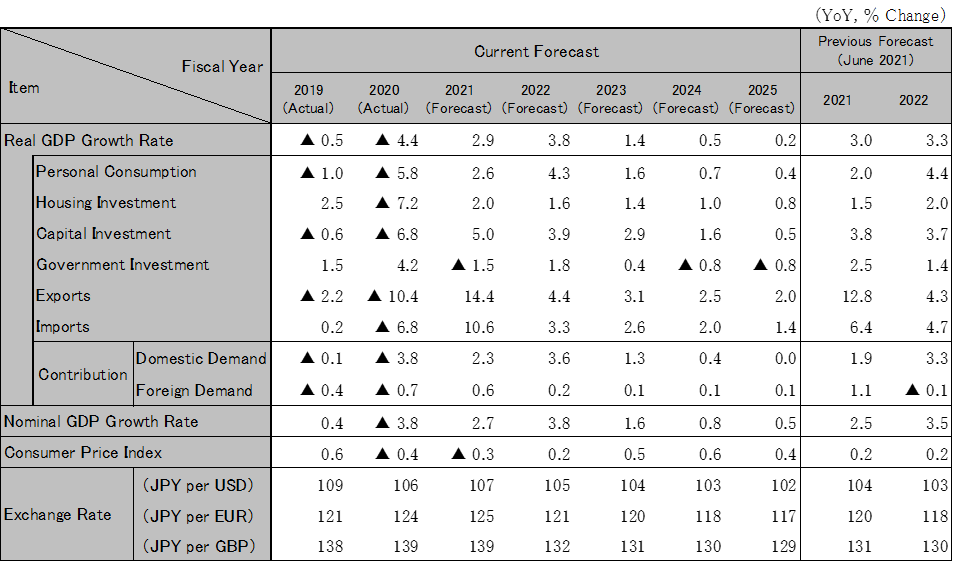

The Japanese economy has been flat due to the reissuance of the declaration of a state of emergency and the expansion of areas covered by the declaration. Meanwhile, the vaccination completion rate has reached 50% and is expected to exceed 70% in November. Going forward, as infections pass the peak and consumption stimulus measures, such as the Go To campaign, are resumed, consumer spending is anticipated to pick up mainly in the service sectors, including food and beverage services, lodging and entertainment. Active exports of capital goods, such as semiconductor manufacturing equipment, and information-related items, mainly to China, will likely continue to be firm. As companies increase their investment in labor-saving and digitalization, mainly in the manufacturing sector, capital investment is expected to continue recovering. The sustainable recovery of the Japanese economy will likely require the continuity of economic measures and policy management. Real GDP growth rate projections are 2.9% in FY2021, and 3.8% in FY2022.

Note: The figures above are calendar-year based. Accordingly, the figures of Japan are different from the fiscal-year based figures in the table below.

Source: IMF. Forecast by Hitachi Research Institute.

Note: The previous forecast for the Consumer Price Index was based on the 2015-year standard, and the current forecast is based on the 2020-year standard.

Source: Japan Cabinet Office, etc. Forecast by Hitachi Research Institute.